Markets

Markets Referral & Affiliate

Referral & Affiliate Rewards

Rewards

Products

Products Support Center

Support Center News

News Research

Research Download

Download English(Australia)

English(Australia)

FameEX Weekly Market Trend | February 13, 2025

2025-02-14 10:46:10

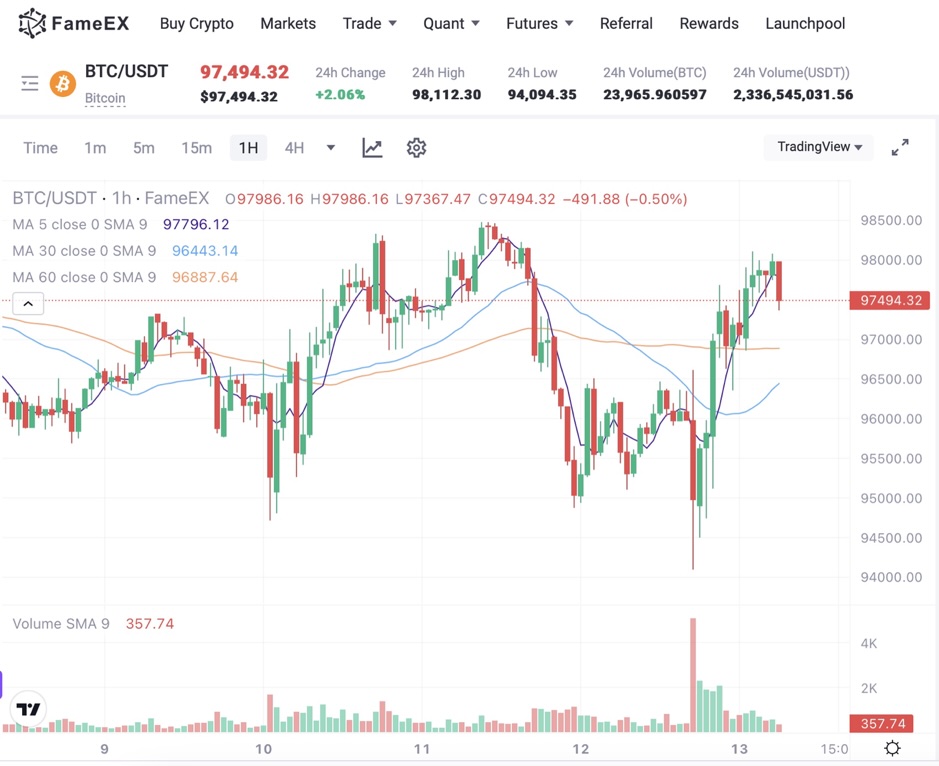

1. BTC Market Trend

From February 10 to February 12, the BTC spot price swung from $94,170.4 to $98,520.49, a 4.62% range.

Key Highlights of Fed Chair Powell’s Semi-Annual Monetary Policy Testimony

1) Interest Rate Outlook: Reaffirmed that there is no urgency to adjust interest rates. If the economy remains strong and inflation does not move toward 2%, a cautious policy stance can be maintained for a longer period. However, if the labor market weakens unexpectedly or inflation declines more than expected, policy adjustments could be made accordingly. Believes the neutral rate has risen.

2) Inflation: Long-term inflation expectations appear stable. While inflation is approaching the 2% target, it remains slightly elevated. The Fed remains focused on achieving its dual mandate. The framework review will not reconsider the inflation target.

3) Labor Market: The unemployment rate remains low and stable. Labor market conditions have cooled from previous overheating but remain solid, without contributing to inflationary pressures. Overall, labor market conditions are balanced.

4) Banking Regulation: Powell reaffirmed the Fed’s commitment to a tailored regulatory approach while preventing excessive burdens on banks. He acknowledged the need to reassess the issue of ‘de-banking’ and emphasized the importance of completing the Basel III implementation

5) Long-Term Interest Rates: The Fed does not control long-term interest rates. Elevated long-term rates are unrelated to Fed policy and are instead determined by supply and demand in the bond market.

6) Tariffs: The Fed maintained the previous stance that economies with free trade grow faster. The Fed does not comment on the tariff policies of the Trump administration.

7) Housing Market: Fannie Mae and Freddie Mac may help lower mortgage rates. However, housing shortages persist even if rates decline. It remains uncertain whether rate cuts would reduce housing inflation.

8) Other Highlights: The closure of the Consumer Financial Protection Bureau (CFPB) would create a gap in consumer compliance protection. The introduction of a central bank digital currency is entirely off the table.

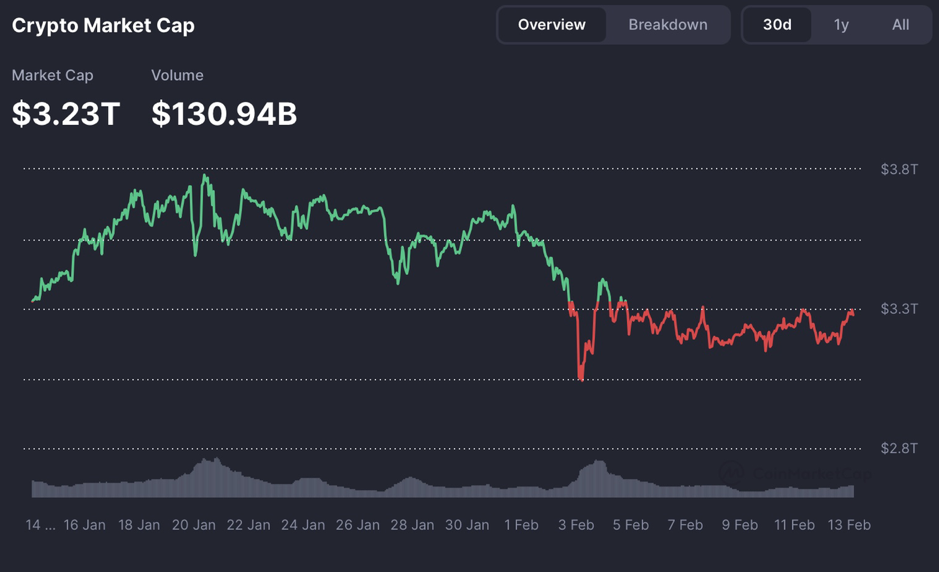

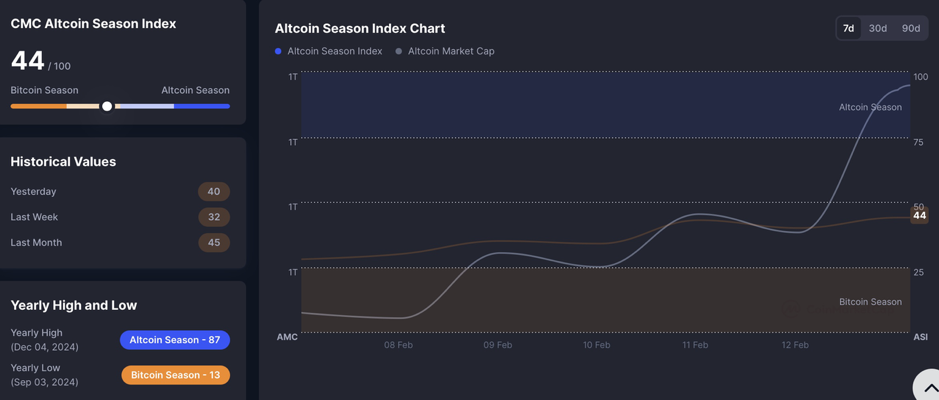

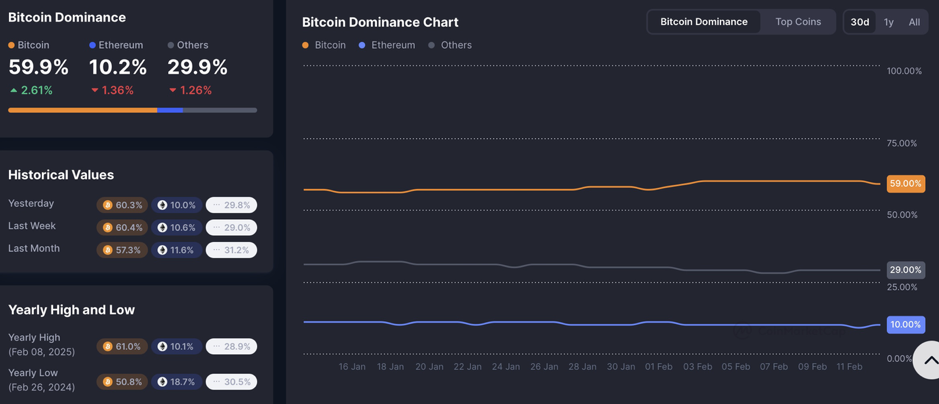

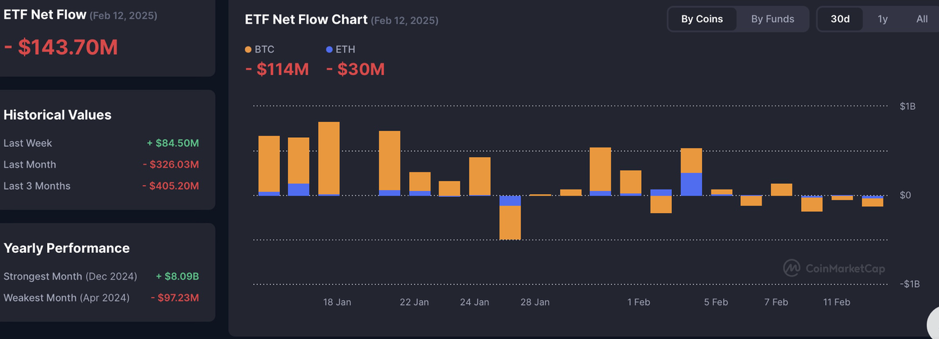

2. CMC 7D Statistics Indicators

Overall market cap and volume, source: https://coinmarketcap.com/charts/

Altcoin Season Index and Bitcoin Dominance: https://coinmarketcap.com/charts/

Crypto ETFs Net Flow: https://coinmarketcap.com/charts/

CoinMarketCap 100 Index: https://coinmarketcap.com/charts/cmc100/

(Used to measure the overall performance of the top 100 cryptocurrency projects by market capitalization on CoinMarketCap)

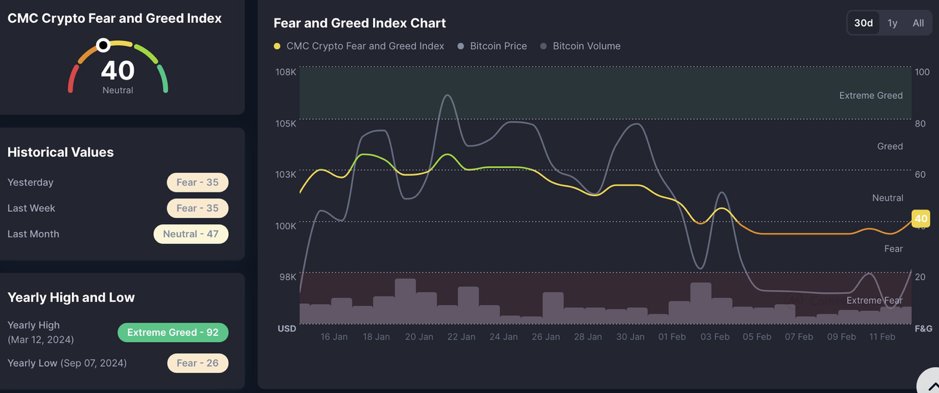

Fear & Greed Index, source: https://coinmarketcap.com/charts/

Based on various statistical indicators, the total market trading volume remains in a downward phase. Altcoin spot prices are generally rising, while ETF net inflows have significantly declined. Large-cap major cryptocurrencies are also experiencing an overall price increase. Market sentiment has started to rebound from its panic bottom.

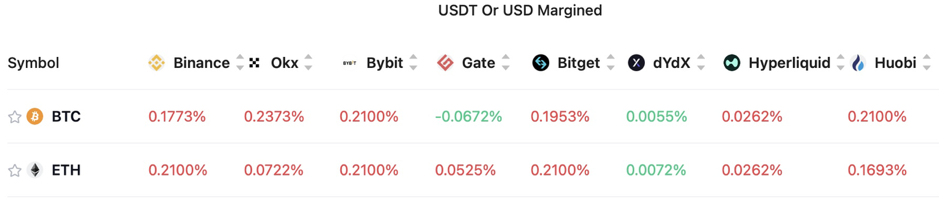

3. Perpetual Futures

The 7-day cumulative funding rates for major exchanges’ mainstream cryptocurrencies are generally positive, indicating that long leverage is currently higher.

Exchange BTC Contract Open Interest:

Exchange ETH Contract Open Interest:

Over the past three days, open interest in BTC and ETH contracts has been steadily increasing, reflecting a rise in short-term market optimism and overall risk appetite.

4. Industry Roundup

1) On February 10, Nasdaq-listed WiMi Hologram Cloud planned to invest $200 million in Bitcoin or cryptocurrency-related securities derivatives. Tesla officially disclosed its BTC holdings, totaling 11,509 BTC, for the first time.

2) On February 10, Japan’s Metaplanet, which shifted from hotel operations to Bitcoin accumulation, saw its stock price surge 4,000% over the past year.

3) On February 10, U.S. regulators launched tokenization pilots using stablecoins as collateral, while European payment giant Klarna is considering cryptocurrency integration.

4) On February 10, Trump and Putin held talks and agreed to negotiate an end to the Russia-Ukraine war. Meanwhile, the Ukrainian government plans to legalize cryptocurrencies before summer.

5) On February 10, Spartan Capital Securities’ Chief Market Economist Peter Cardillo stated that if inflation persists for another one to two months, the Fed may not cut rates this year. Former U.S. Treasury Secretary Larry Summers warned of potential inflation resurgence, suggesting the Fed’s next move could be a rate hike.

6) On February 10, it was said that the Trump administration is considering merging the FDIC and OCC to reduce banking regulatory powers. Rumors suggest Elon Musk plans to spend $40 million on a Super Bowl ad focused on DOGE and government waste.

7) On February 10, Bloomberg reported that Wall Street’s major banks are expanding into crypto, anticipating IPO opportunities under a potential Trump administration. Goldman Sachs’ Bitcoin ETF holdings increased to $1.5 billion in Q4 2024.

8) On February 10, Mali, one of Africa’s largest gold producers, saw gold production plummet by 23% in 2024.

9) On February 11, PitchBook reported that crypto venture funding in 2024 has reached $10 billion, nearly matching 2023 levels.

10) On February 11, Nasdaq submitted 19b-4 applications for CoinShares’ Litecoin ETF and XRP ETF.

11) On February 11, spot gold prices surged above $2,930/oz, rising 0.76% intraday and over 11% year-to-date, while NY gold futures reached $2,955.50/oz.

12) On February 11, EU Commission President Ursula von der Leyen stated that the EU would take firm and proportionate countermeasures against U.S. tariffs.

13) On February 11, FTX creditors claimed that if SBF had not filed for bankruptcy, FTX’s assets could have exceeded $65 billion. FTX’s first repayment phase is expected to reach $6.5–7 billion.

14) On February 11, Federal Reserve officials shifted their stance, signaling a more favorable regulatory environment for the crypto industry.

15) On February 11, Ukrainian President Volodymyr Zelensky stated that he is prepared to propose exchanging territory captured by the Ukrainian military in last year’s offensives in the Kursk region for Ukrainian land under Russian control to end the Russia-Ukraine conflict.

16) On February 12, the U.S. January unadjusted CPI annual rate recorded 3%, exceeding the expected 2.90% and the previous 2.90%, marking the largest increase since June 2024.

17) On February 12, the U.S. January seasonally adjusted core CPI monthly rate recorded 0.4%, surpassing the expected 0.30% and the previous 0.20%, marking the largest increase since March 2024.

18) On February 12, U.S. President Donald Trump stated that interest rates should be lowered, emphasizing that rate cuts would complement the upcoming tariff policies. He also dismissed claims that J.D. Vance is his presidential successor.

19) On February 12, Saudi Arabia’s “Neom” project secured a $5 billion investment to establish an artificial intelligence data center, while France announced plans to invest over €100 billion in the AI sector.

20) On February 12, Federal Reserve Chairman Jerome Powell called for a “reassessment” of the de-banking issue in the crypto industry and stated that a central bank digital currency would not be pursued during his tenure.

21) On February 12, the U.S. SEC stated that it would not finalize a cryptocurrency regulatory agenda before confirming a new chairman.

22) On February 12, Hong Kong confirmed that Bitcoin and Ethereum can be used as proof of wealth for investment visas. Meanwhile, Japan’s Financial Services Agency plans to classify cryptocurrencies as financial products similar to securities.

23) On February 12, the memecoin and AI token index plunged 50% from its December peak, while the U.S. concept and DeFi index have shown relative resilience.

24) On February 12, Tether announced a strategic investment in the self-custody crypto wallet Zengo Wallet.

25) On February 12, the most hawkish member of the Bank of England stated that downside risks from weak demand outweigh inflation risks and expressed support for significant rate cuts.

5. Market Outlook

From February 13 to February 16, keep monitoring ETH spot trading opportunities. The sell order at $5,125, along with the buy orders at $2,040 and $1,730, should remain active. For the BTC spot, maintain the sell order at $169,400 and the buy orders at $73,970, $59,935, and $45,900.

Risk Reminder: Cryptocurrency investments are highly volatile, with significant price fluctuations and speculative risks. The above content is for reference only and does not constitute specific investment advice from this exchange.

Disclaimer: FameEX makes no representations on the accuracy or suitability of any official statements made by the exchange regarding the data in this area or any related financial advice.